Investment

₹

Posted On Monday, Apr 07, 2025

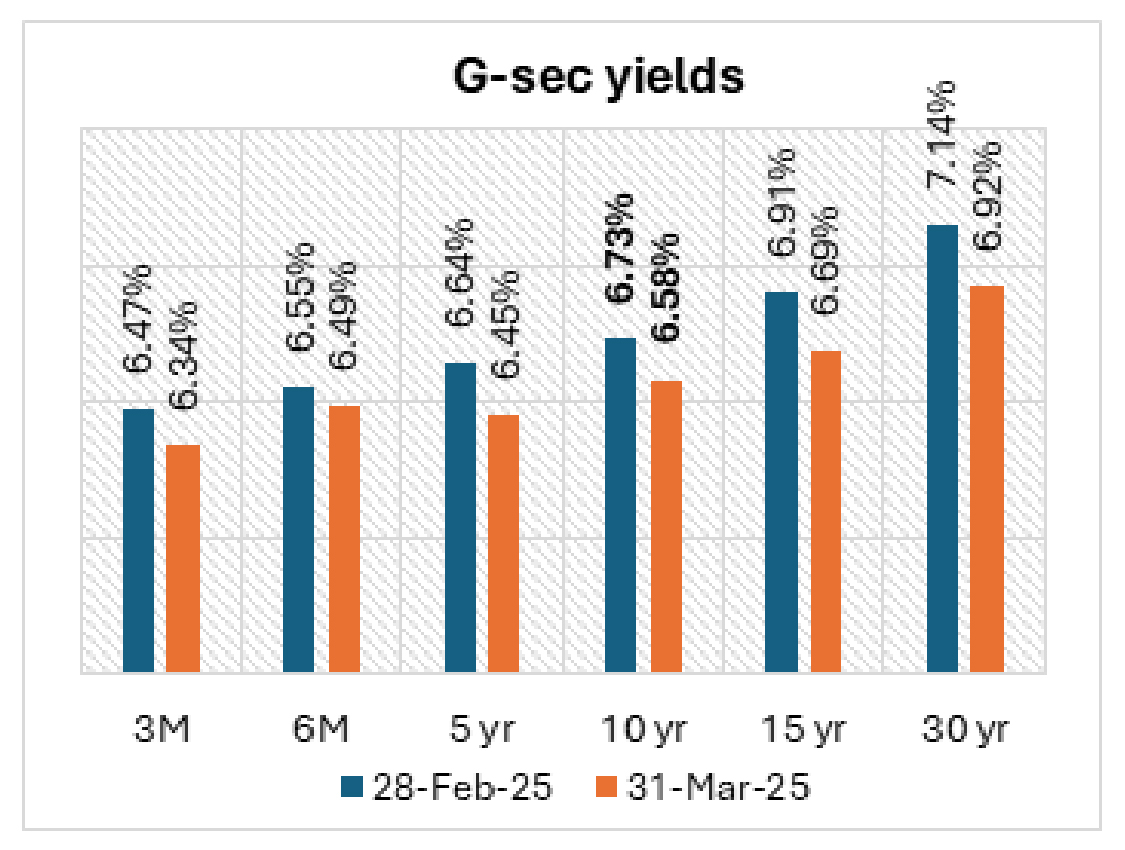

In March 2025, both U.S. Treasury and Indian Government Bond yields cooled off, influenced by a blend of global and domestic factors. President Trump’s aggressive tariff announcements spooked markets, driving investors to safer assets like U.S. Treasuries. At the same time, expectations of U.S. rate cuts and risk to growth outlook, fueled by weak economic data, added further pressure on Treasury yields.

On the domestic front, the RBI took proactive steps to improve liquidity through Open Market Operations (OMO) and currency swaps, leading to easing in the Indian Government Bond (IGB) yields.

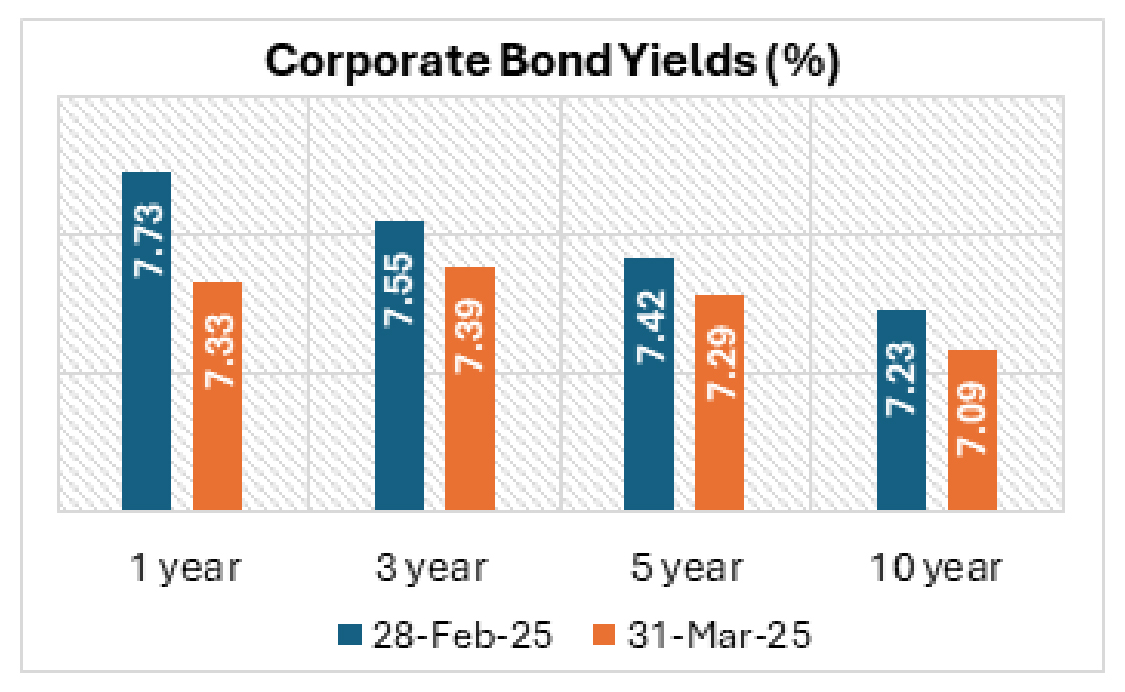

In the money market, T-bill rates for the 3-month segment plunged post easing in liquidity conditions. Meanwhile, the 3-month AAA PSU CP/CD rates too moved in tandem to the 7.2%- 7.3% range against the 7.45% - 7.50% band on closing basis. The corporate bond yield curve continues to show strong demand in the 5–7-year segment.

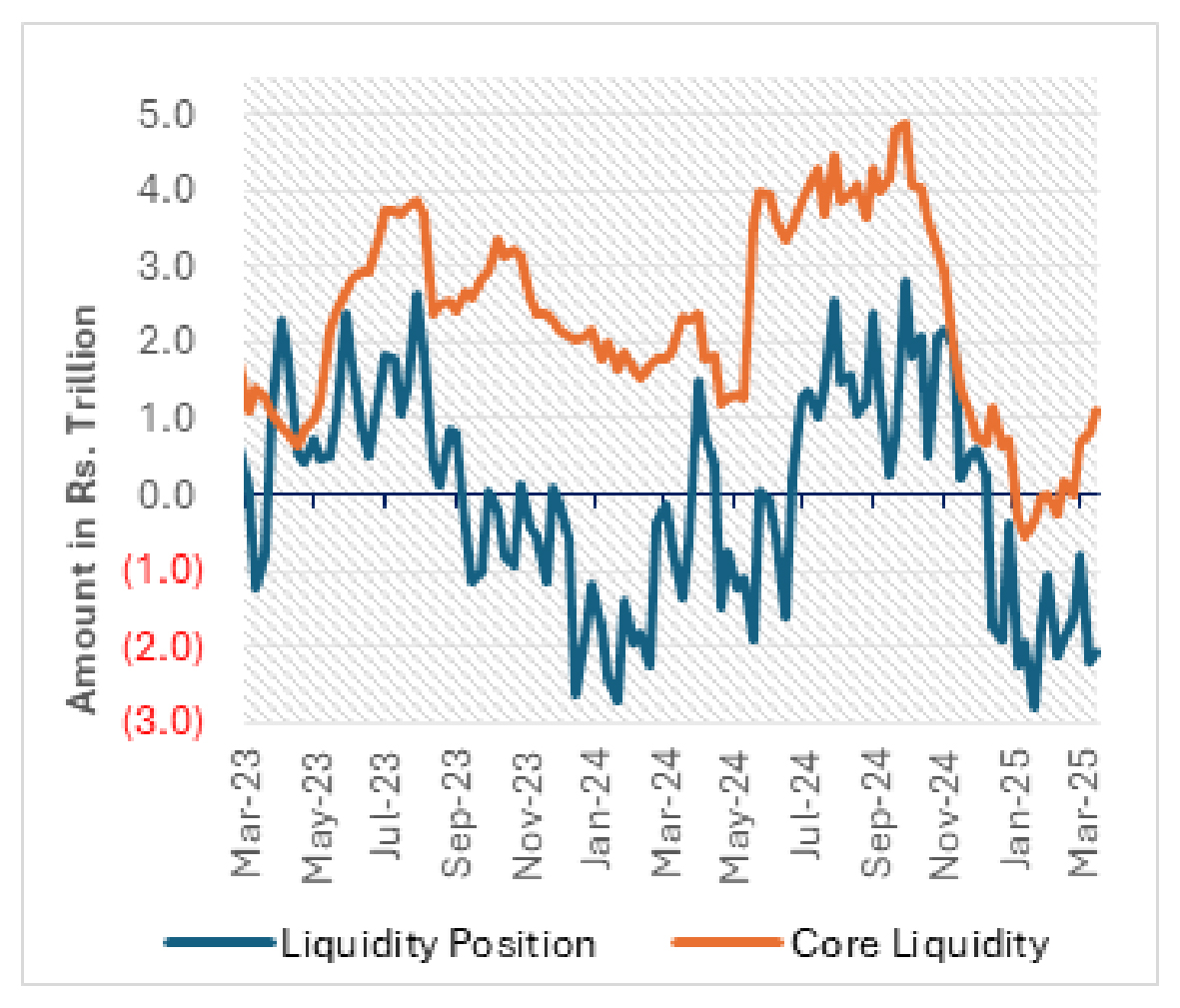

Banking system liquidity eased in March 2025 despite seasonal pressures from advance tax, GST, excise collections, and currency demand. The RBI offset these challenges with significant OMO purchases, pushing core liquidity into surplus. The average daily deficit stood at Rs 1.6 trillion for the month. To facilitate smooth transmission of rate cuts, the RBI actively managed liquidity through a Rs 800 billion OMO purchase program for April 2025 (to be effective in four tranches of Rs 200 billion each), along with other measures like a $10 billion dollar-rupee swap auction. Since January 2025, total OMO purchases have reached Rs 3.30 trillion. As a result, core liquidity surged into a surplus of Rs 1.1 trillion by March 21, 2025.

Liquidity conditions are likely to improve in the coming months, as we expect the RBI to remain proactive in managing liquidity. Early April 2025 will likely see strong spending, following past trends, and will be further supported by a large RBI dividend of Rs 2.5-3 trillion expected in May 2025. This should ensure ample liquidity in the first half of the year. However, currency demand and seasonal changes in government balances could lead to tighter conditions in the second half.

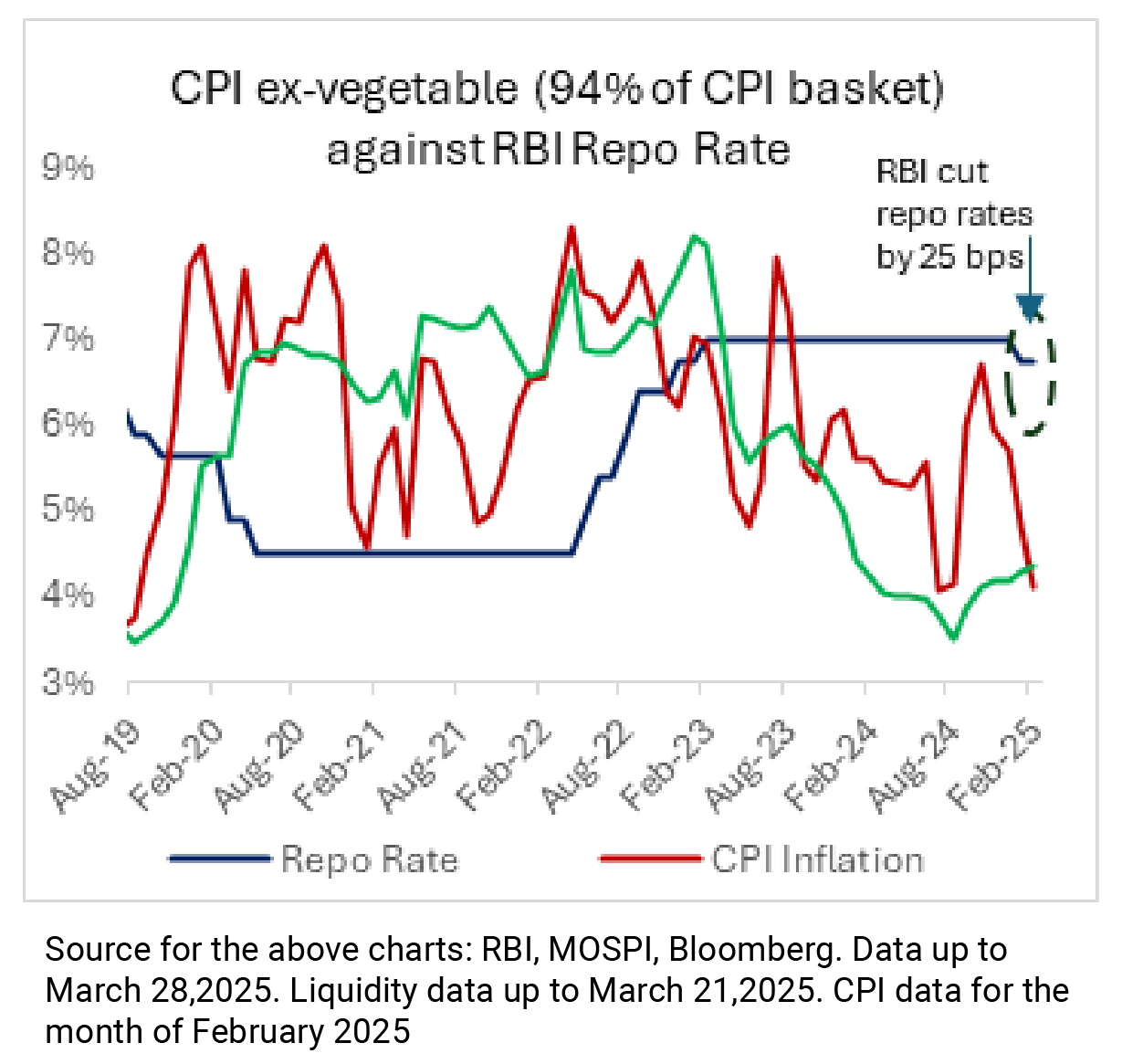

The headline Consumer Price Index (CPI) inflation has significantly eased from 5.2% YoY in December 2024 to 3.61% YoY in February 2025. Food inflation has shown a notable decline, dropping from 7.69% YoY in December 2024 to 3.84% YoY in February 2025. In contrast, core inflation has slightly risen to 3.99% YoY, primarily driven by gold prices.

In our estimates, March 2025 inflation is trending toward the ~3.5% range. With ongoing food disinflation and stable global oil prices, we expect headline inflation to align with the RBI's forecast of 4% for Q4 FY26.

Globally, U.S. 10-year Treasury yields dropped from 4.21% to 3.94% following President Trump's announcement of aggressive global tariffs in early April 2025. The tariff news caused market disruption, prompting investors to flock to safe-haven assets like U.S. Treasuries, which led to a decline in yields. Additionally, expectations of rate cuts by the U.S. Federal Reserve, driven by weak manufacturing data and concerns about a potential slowdown in growth, further contributed to the fall in Treasury yields.

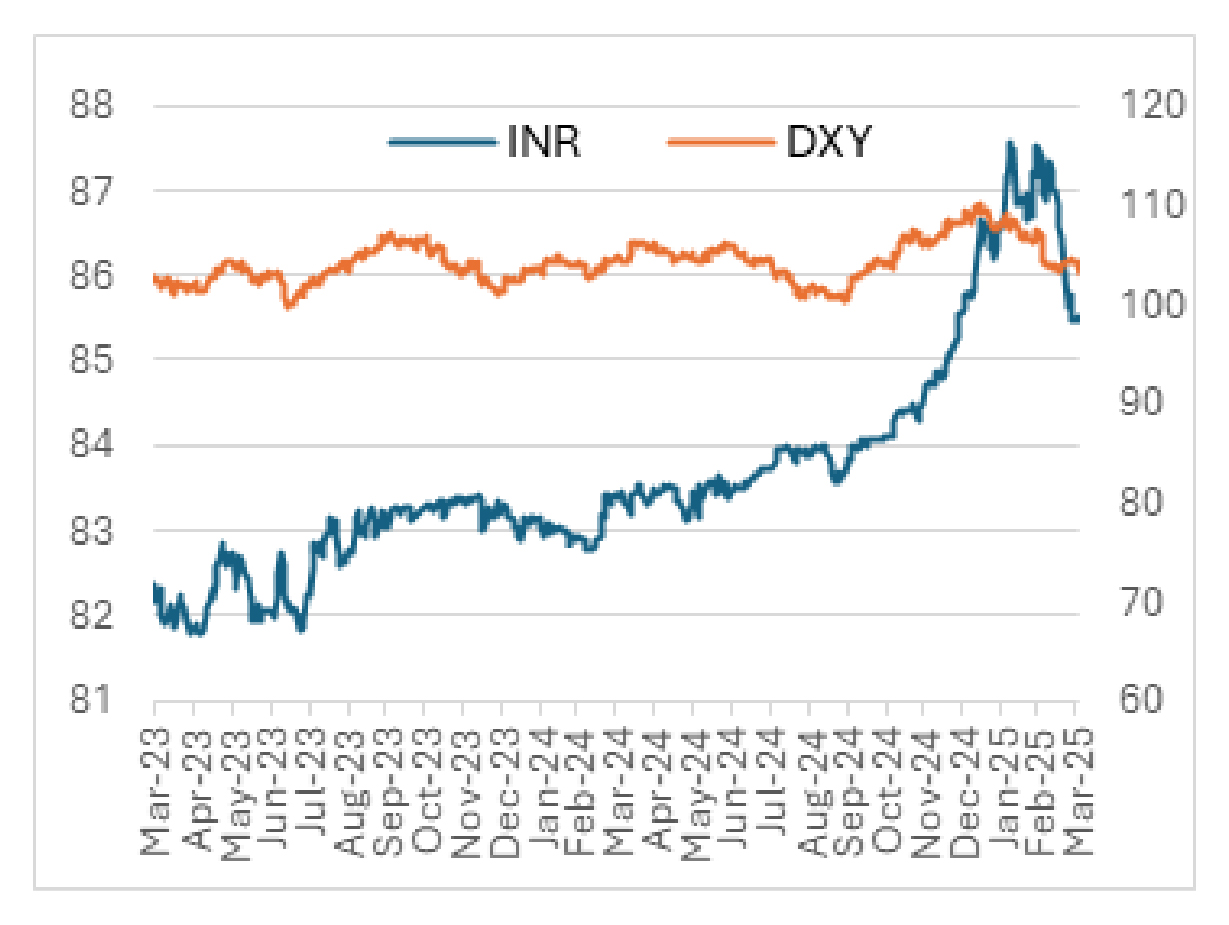

The Indian Rupee (INR) appreciated by 2.33% against the U.S. Dollar on a month-on-month basis, strengthening from Rs 87.5/USD in February 2025 to Rs 85.5/USD in March 2025. This appreciation was driven by a combination of factors, including a rise in foreign investments, a weaker U.S. dollar amid escalating trade tensions, effective liquidity management by the RBI, and the rupee’s resilience in a volatile global market.

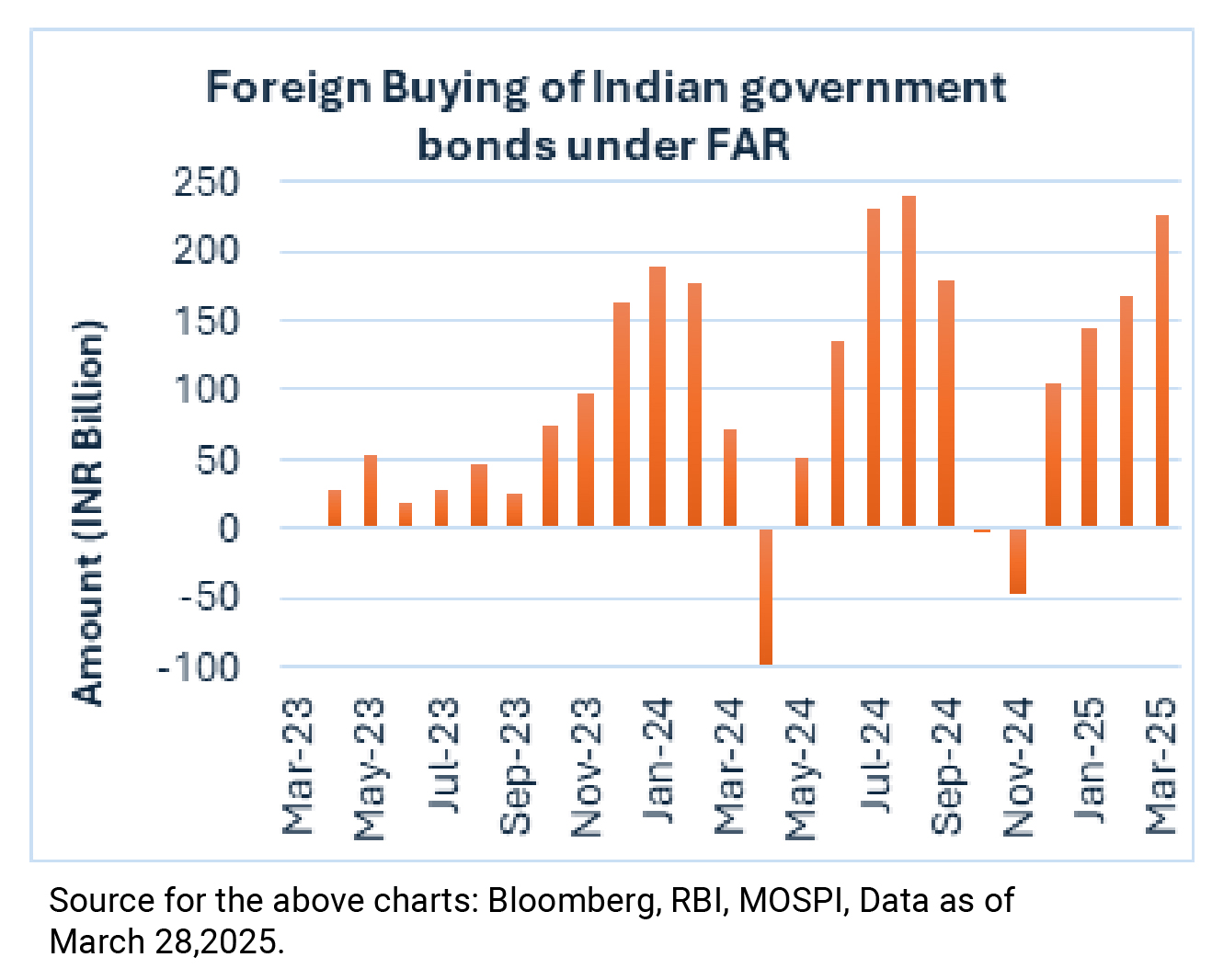

Foreign investments in IGBs saw notable growth in March 2025 alone, with the Fully Accessible Route (FAR) segment receiving an influx of Rs 227 billion during the month alone.

In the medium term, global financial markets are expected to experience reduced volatility. The USD is likely to stabilize within its current range, potentially leading to a reversal of the safe-haven trade, which may result in increased capital flows into Emerging Markets (EMs).

The Reserve Bank of India's Monetary Policy Committee (MPC) is scheduled to meet from April 7-9, 2025, marking its first meeting for the fiscal year 2025-2026.

We expect a 25-basis point rate cut, lowering the repo rate to 6% at the April 2025 MPC meeting. With liquidity likely to stay in surplus, market participants are increasingly anticipating the RBI to adopt an "accommodative" policy stance in April 2025. However, given the ongoing global uncertainty and the lack of clarity surrounding the domestic monsoon—which could offer insights into food inflation trends—we believe the Committee may decide not to change the policy stance in the April meeting.

Given the RBI's clear intent to sustain a healthy liquidity surplus, we anticipate a gradual increase in core liquidity to at least 1% of Net Demand and Time Liabilities (NDTL), designed to ensure smoother transmission of rate cuts. At this point, we view an official change in stance as largely a formality. As a result, we anticipate continued active liquidity management by the RBI. We also see a greater likelihood of an additional 25 bps rate cut in the June 2025 policy, contingent on the evolving growth-inflation dynamics and considering the RBI's pro-growth approach.

India’s GDP growth for Q3FY25 hit 6.2% YoY, driven by strong government spending, private consumption, and robust exports. However, concerns over a potential global growth slowdown persist, with weakening U.S. economic data adding to the uncertainty. Expectations of softer crude prices and India's fiscal and liquidity measures provide a foundation for continued economic stability.

Owing to these developments and uncertainties, we expect the markets to experience some volatility in the near term. However, we maintain our medium-term positive outlook (refer Bull Case Revisited) on long-term bonds considering:

• Declining net supply of government bonds.

• Continued strong demand from insurances companies, pension and provident funds

• India’s inclusion in the global bond indices to continue to add to the demand

• Potential rate cuts and Open Market Operations (OMO) purchases by the RBI

Given the above factors, we expect the bond yields to go down (prices to go up). In this declining interest rate environment, investors with medium to long investment horizon, should consider dynamic bond funds. These funds can allocate to long-duration bonds while keeping flexibility to adjust portfolio position if market conditions change. This adaptability allows investors to remain invested for a longer period.

For investors with shorter investment horizons and a low risk tolerance, liquid funds remain the more suitable option.

Source: Reserve Bank of India (RBI), Ministry of Statistics & Programme Implementation (MOSPI), Bloomberg

|

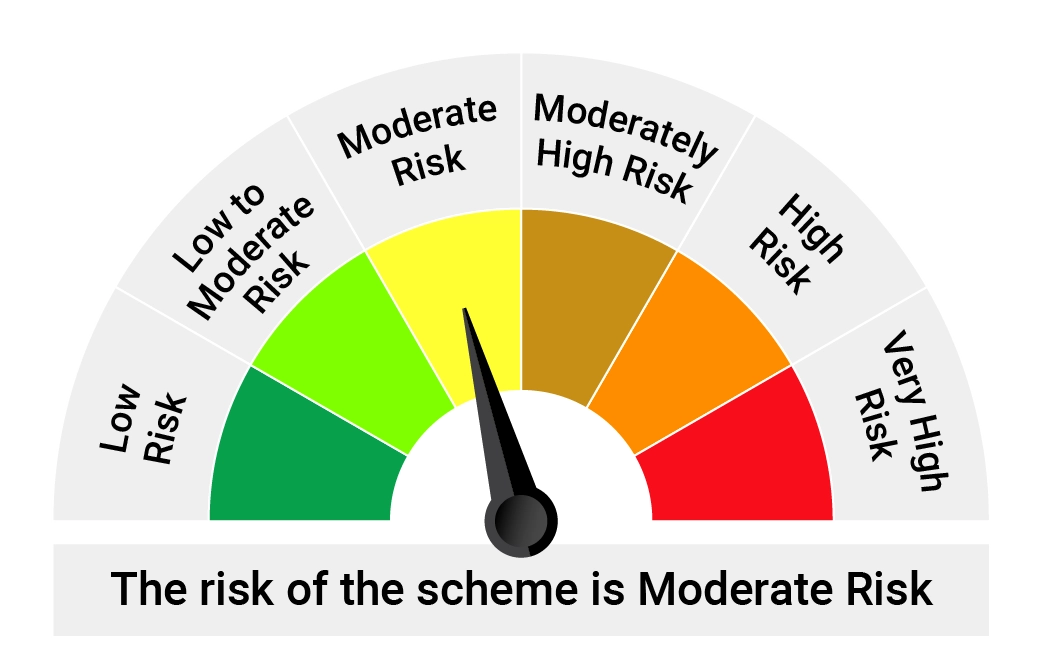

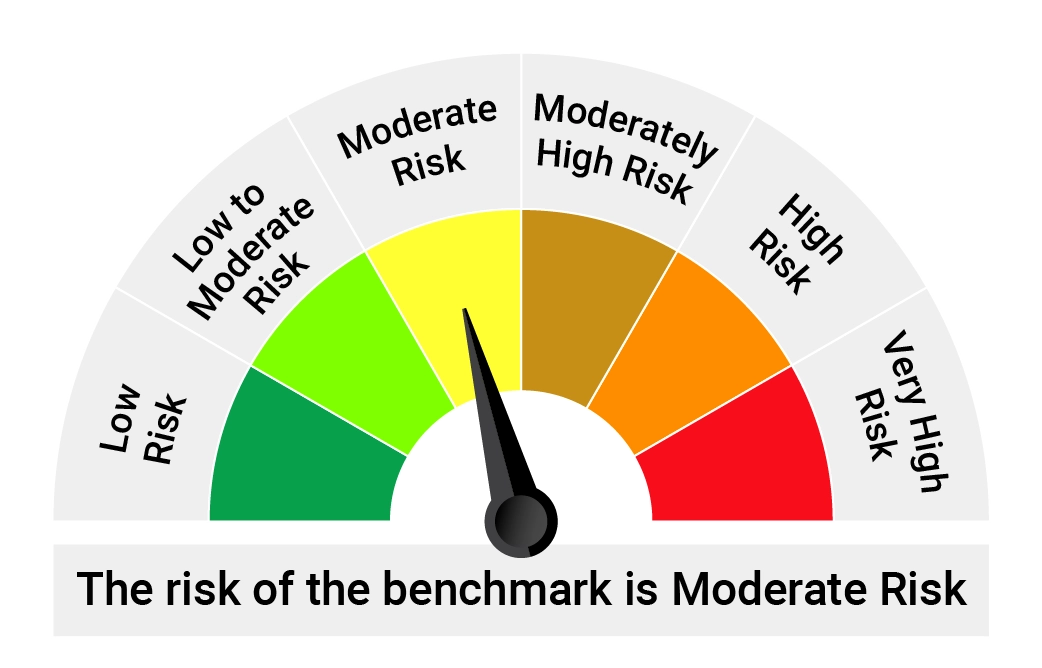

| Name of the Scheme and Benchmark | This product is suitable for investors who are seeking* | Risk-o-meter of Scheme | Risk-o-meter of Tier-I Benchmark |

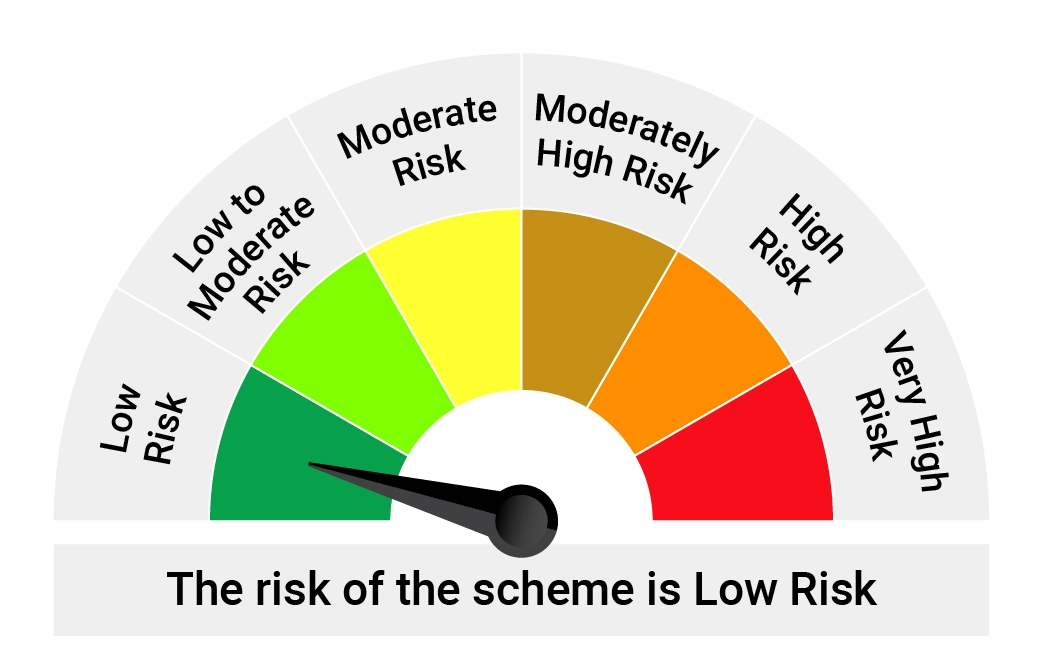

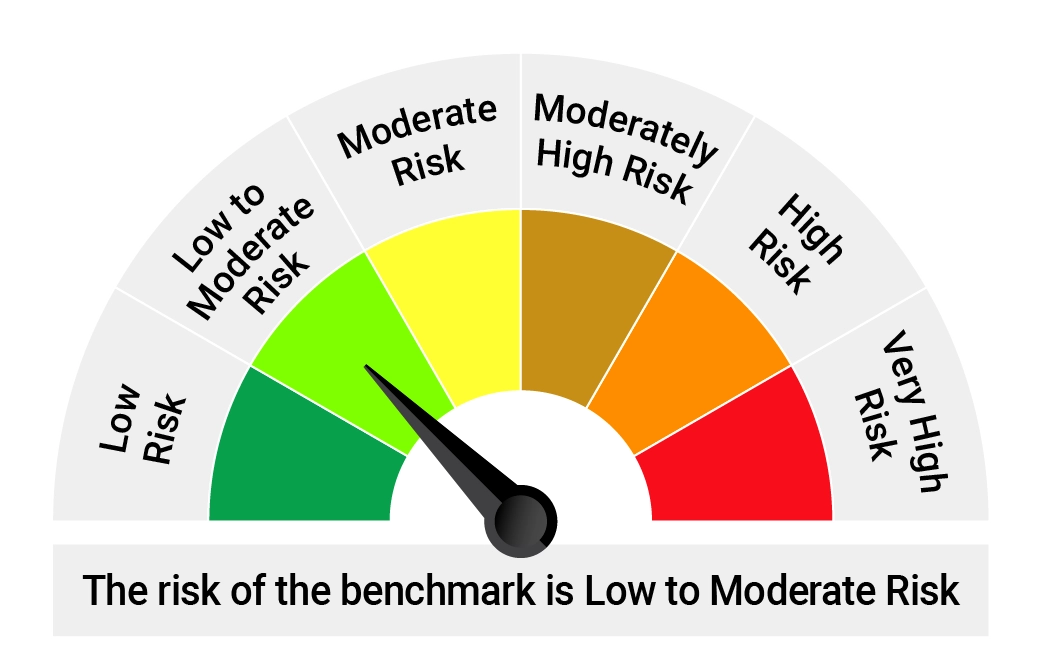

Quantum Liquid Fund An Open-ended Liquid Scheme. A relatively low interest rate risk and relatively low credit risk Tier I Benchmark : CRISIL Liquid Debt A-I Index | • Income over the short term • Investments in debt / money market instruments |  |  |

Quantum Dynamic Bond Fund An Open-ended Dynamic Debt Scheme Investing Across Duration. A relatively high interest rate risk and relatively low credit risk. Tier I Benchmark : CRISIL Dynamic Bond A-III Index | • Regular income over short to medium term and capital appreciation • Investment in Debt / Money Market Instruments / Government Securities |  |  |

| Potential Risk Class Matrix – Quantum Liquid Fund | |||

Credit Risk → | Relatively Low | Moderate (Class B) | Relatively High (Class C) |

Interest Rate Risk↓ | |||

| Relatively Low (Class I) | A-I | ||

| Moderate (Class II) | |||

| Relatively High (Class III) | |||

| Potential Risk Class Matrix – Quantum Dynamic Bond Fund | |||

Credit Risk → | Relatively Low | Moderate (Class B) | Relatively High (Class C) |

Interest Rate Risk↓ | |||

| Relatively Low (Class I) | |||

| Moderate (Class II) | |||

| Relatively High (Class III) | A-III | ||

*Investors should consult their financial advisers if in doubt about whether the product is suitable for them.

Disclaimer, Statutory Details & Risk Factors:The views expressed here in this article / video are for general information and reading purpose only and do not constitute any guidelines and recommendations on any course of action to be followed by the reader. Quantum AMC / Quantum Mutual Fund is not guaranteeing / offering / communicating any indicative yield on investments made in the scheme(s). The views are not meant to serve as a professional guide / investment advice / intended to be an offer or solicitation for the purchase or sale of any financial product or instrument or mutual fund units for the reader. The article has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate and views given are fair and reasonable as on date. Readers of this article should rely on information/data arising out of their own investigations and advised to seek independent professional advice and arrive at an informed decision before making any investments. Mutual Fund investments are subject to market risks, read all scheme related documents carefully. |

Posted On Monday, Apr 07, 2025

In March 2025, both U.S. Treasury and Indian Government Bond yields cooled off

Read More

Posted On Friday, Mar 07, 2025

February 2025 kicked off with two key events in Indian bond markets: the Union Budget and RBI's Monetary Policy.

Read More

Posted On Friday, Feb 07, 2025

Bond markets witnessed increased volatility during the last month with the 10-year Government

Read MoreGet In Touch

Take small steps in your financial planning to achieve big dreams! Start your investment journey today!