Investment

₹

Posted On Wednesday, Jun 22, 2022

Bond Markets run ahead of Central Banks. Time to allocate to Indian Bonds.

The US treasury secretary John Connally proclaimed at the G-10 meeting held in Rome in late 1971 - “The dollar is our currency, but it’s your problem”.

50 years have passed since, but the movements in the US dollar continue to worry policymakers across the world. The US economy is about a quarter of the world GDP. The US Dollar is used for the settlement of over 40% of all international trades and it accounts for about 60% of total central bank reserves worldwide.

Thus, whatever the FED does to the US interest rates and hence its impact on the US Dollar has repercussions for the entire world.

It gets even more troubling, at a time when the Federal Reserve (FED) is fighting the highest inflation in the US, in 40 years.

FED’s inflation fight

On June 15, 2022, the FED hiked the federal funds rate (the interest rate at which commercial banks borrow and lend their overnight excess reserves) by 75 basis points, the largest one-off rate hike since 1994.

Since March this year, the federal funds rate has been raised by a cumulative 150 basis points from the range of 0%-0.25% to 1.50%-1.75%.

CPI inflation in the US is still above 8% and the US economy is creating about two jobs for every single person looking out for a job. So, the FED has every reason to continue hiking rates till they get inflation under control. To recall, the FED targets to keep inflation at 2%.

As per FED’s own projection, the federal funds rate will be at 3.4% by December 2022. This implies another 175 basis points rate hike over the next six months.

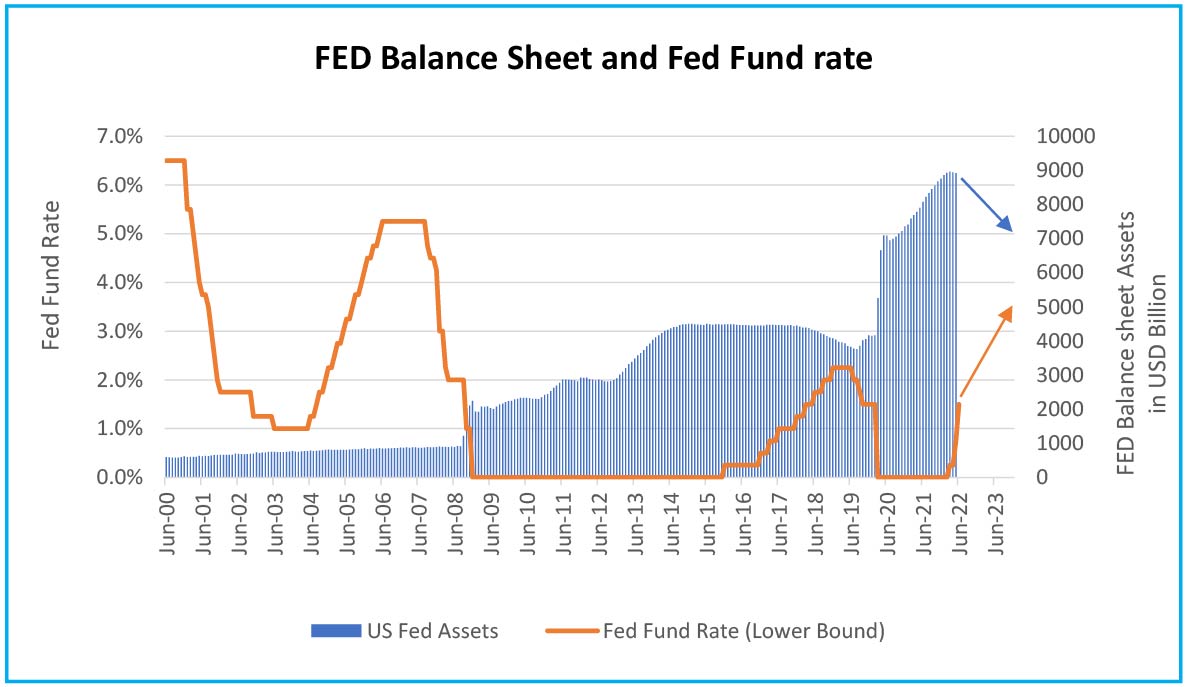

Alongside, the Fed has also started the process to reduce its gigantic USD 9 trillion balance sheet by letting the bonds in its portfolio mature and not reinvest the money. The pace of balance sheet runoff is set at USD 47.5bn per month until September when it will ramp up to a total of USD 95bn per month.

At this pace, FED’s balance sheet assets will fall by USD 1.6 trillion by the end of 2023. This means the Fed will take away USD 1.6 trillion of liquidity from the global financial system.

Chart – I: US FED intends to hike the interest rate by over 300 basis points and take out USD 1.6 trillion of liquidity

Source – Bloomberg, Quantum Research; Data as of June 2022

Past Performance may or may not sustained in future.

We all know how lower interest rates and a flood of global liquidity have helped risk assets like equities and long-term bonds over the last many years. So, reversal of these conditions would obviously have a negative impact on these assets.

This year, as of June 17, 2022, the US equity index S&P 500 is down 23%; during the same time, the 10-year US treasury yield is up 171 basis points (1%=100 basis points). The Bloomberg US Aggregate Bond Index which comprises US treasury and investment-grade bonds, is down 11.5% in absolute terms, year to date.

A similar trend in equities and bonds performance can be seen across all major economies. In India, BSE Sensex is down ~12% and the 10-year government bond yield is up 110 basis points. The Crisil Composite Bond Fund Index is down 2.3% in INR terms and down by about 6.9% in USD.

Peak Inflation Narrative

The mood on street is extremely pessimistic. The pace at which the FED and many other central banks are moving has frightened investors.

At this point, the biggest question on top of the investor’s mind is – How far will the FED go?

The FED expects that a FED Funds rate averaging 3.5% over the next 2 years will be enough to get inflation back to its 2% range with some growth sacrifice but no major increase in unemployment. This is what they term, a soft landing.

While on the other hand, if PCE inflation (FED’s preferred measure) falls only to say 4% in 2023 from the current levels of 5.5%, it would force the FED to hike way more than current expectations and tighten its balance sheet at a faster pace forcing the economy into recession. A hard landing.

So, the simple answer to the above question is that we don’t know. And neither does the Federal Reserve nor the Reserve Bank of India.

Times are uncertain and hence, investing has to accommodate probabilities, some base assumptions, and the ability to react. And it is necessary to remain objective during this volatile time.

As things stand now, it seems that the narrative around the inflation fight, and the monetary policy tightening is peaking now, though the FED has to catch up with it.

The bond market has built-in significant uncertainty premium. So, if things do not worsen from here, we may see the global bond and currency markets stabilising or possibly improving from current levels.

What does this mean for Indian Bonds?

Monetary tightening (liquidity withdrawals and rate hikes) in the developed world typically causes capital outflows from emerging markets (EM) and puts pressure on EM currencies, which then transmits to the domestic bonds.

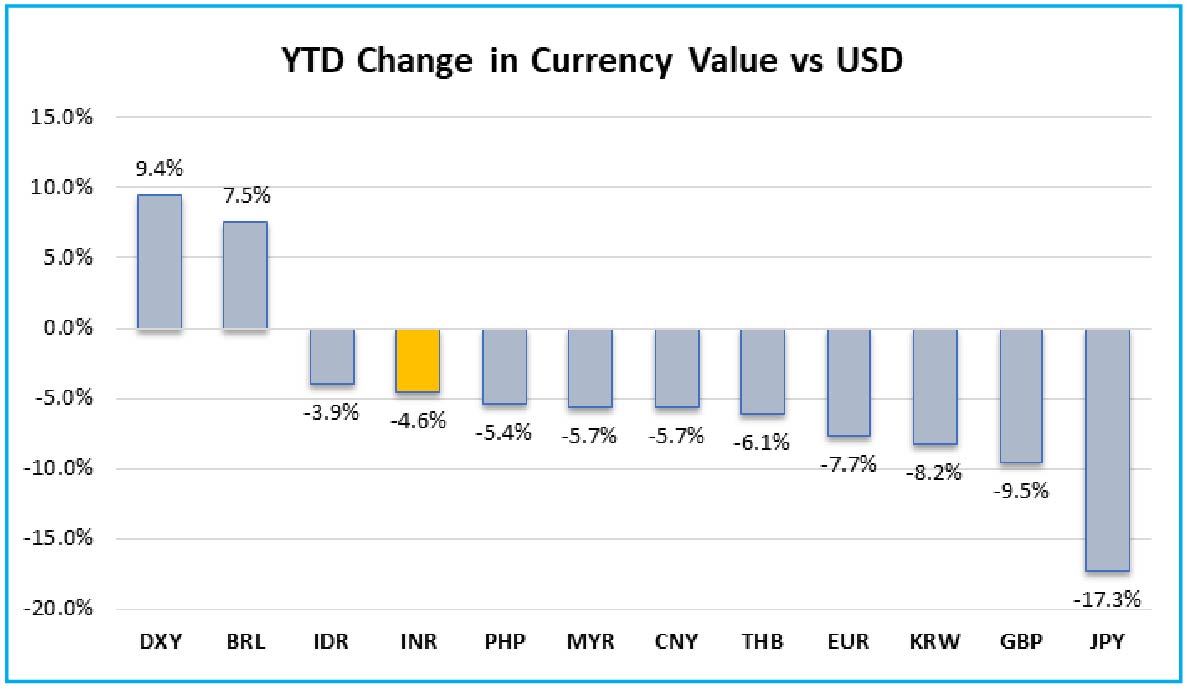

In the 2022 year till date (June 17, 2022), the Dollar Index has risen by 9.44% while the INR has weakened against the US dollar by only 4.57%. Consequently, the INR has appreciated against most of the major currencies during this period.

Chart – II: INR depreciated lesser than most major currencies

Source – Bloomberg, Quantum Research; Data as of June 17, 2022

Past Performance may or may not sustained in future.

This relative outperformance in the INR has come despite the fact that the foreign portfolio investors have sold more than USD 28 billion of Indian Equities and bonds since the start of the year 2022.

Despite these outflows and a higher currency account deficit, The RBI is still sitting with USD 596 billion of foreign exchange reserves as of June 10, 2022. It also has over USD 63 billion of long dollar position (to be purchased at future date) in the forward market. This gives the RBI enough firepower to protect against any sharp selloff in the Indian Rupee.

This is comforting for the Indian bond markets. High forex reserves provide flexibility to the RBI to focus on domestic growth inflation balance. Though Indian currency and bonds may not be immune to the FED tightening, a high FX buffer will surely reduce its sensitivity.

Bond valuation getting attractive

This year so far, the RBI has raised the policy repo rate (the interest rate at which banks borrow from the RBI) by cumulative 90 basis points from 4.0% to 4.9%. Taking into account the introduction of the standing deposit facility (Quantum Policy Commentary), the effective overnight interest rate has been hiked by 130 basis points from 3.35% to 4.65%.

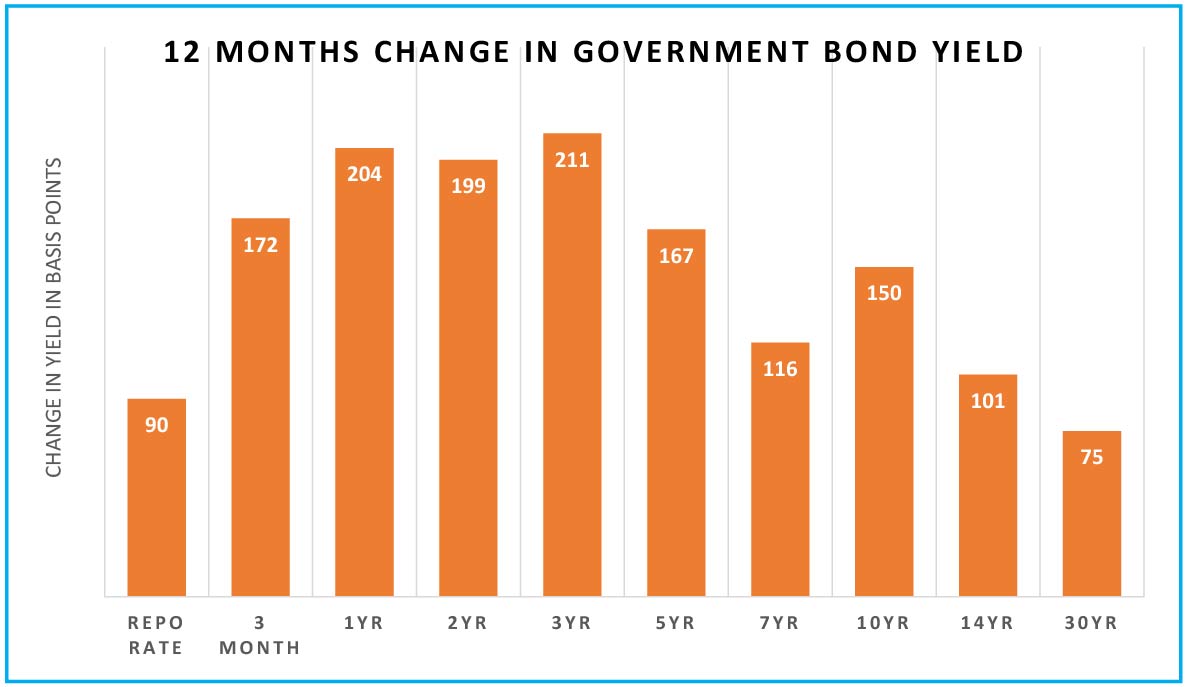

Indian bond yields have been on the rise for the last 12 months; tracking international crude oil prices, global yields, domestic inflation pressures, and adverse demand-supply balance. The 10-year government bond yield is higher by 150 basis points, while the 2-year bond yield is up 200 basis points.

Chart - III: Bond Yields moved up ahead of RBI rate hikes

Source – Refinitiv, Quantum Research; Data as of June 17, 2022

Past Performance may or may not sustained in future.

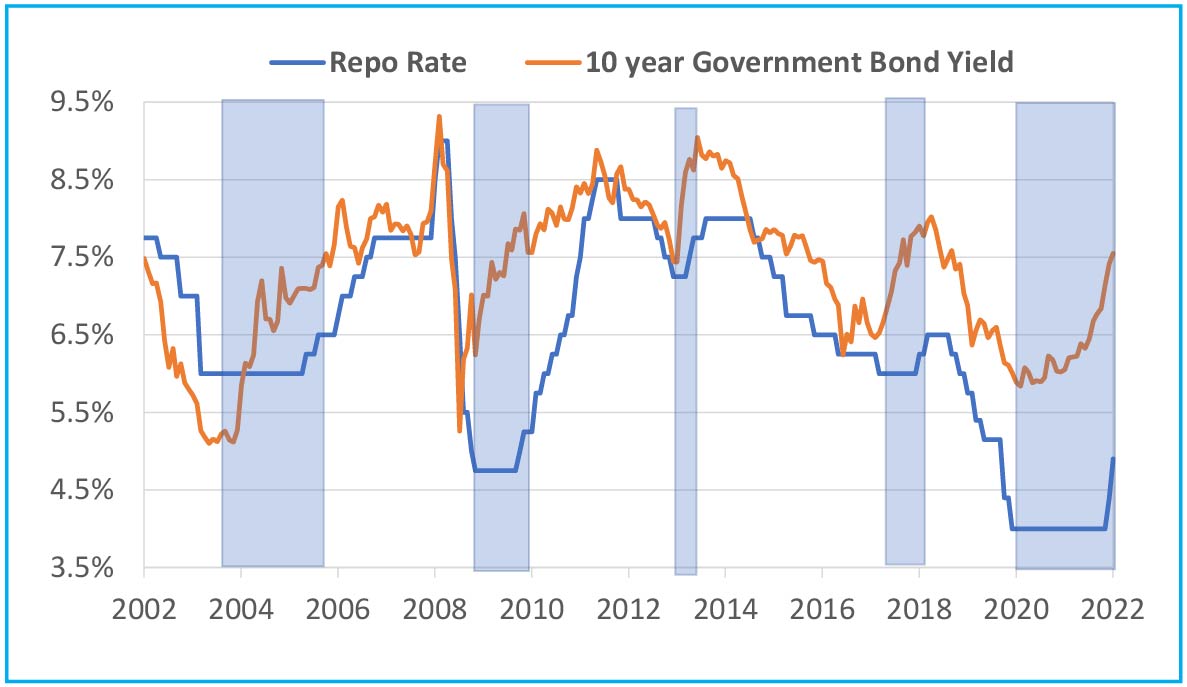

Currently, the 10-year government bond yield is trading at 7.54%, while the 3-year government bond is trading at 7.0%. Most of the medium to long-duration bonds are trading at a yield higher than their December 2018 levels when the repo rate was at 6.50%.

Bond markets have a tendency to pre-empt policy moves. In all the previous rate hiking cycles, the maximum rise in yields had happened up until the first-rate hike. Thereafter, yields moved up only marginally or got stuck in a narrow range.

Chart - IV: Bond Yields move ahead of the Policy rates

Source – Refinitiv, Quantum Research; Data as of June 17, 2022

Past Performance may or may not sustained in future.

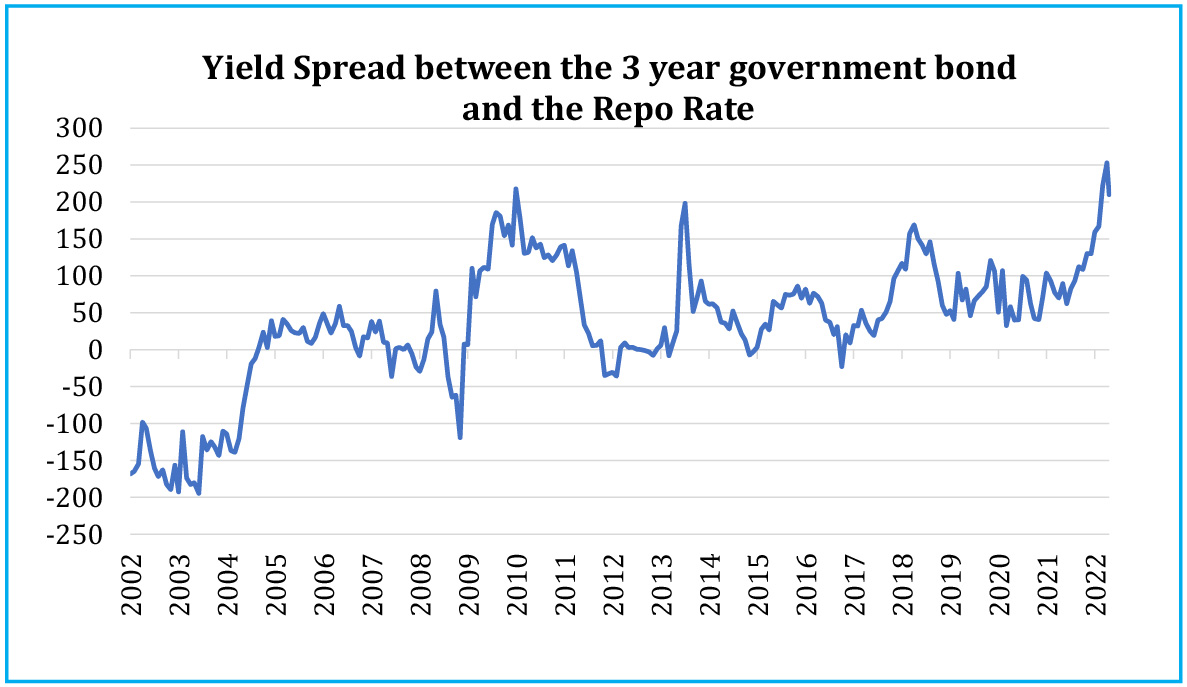

The 3-year government bond is currently trading at 210 basis points above the policy repo rate. The long-term average of this spread in a tightening interest rate environment is ~80 basis points.

Chart - V: Bond Valuations have built-in significant uncertainty premium

Source – Refinitiv, Quantum Research; Data as of June 17, 2022

Past Performance may or may not sustained in future.

Some of the widening in term spreads is due to a wider fiscal deficit and increased supply of bonds. Still, at this valuation, the 3-5 year part of the bond yield curve has already built in a significant uncertainty premium. Much of the domestic rate hikes are also priced in. Thus, the bond market may not be too sensitive to RBI’s rate hikes going forward.

However, high uncertainty over global monetary policy, rising crude oil prices, and unfavourable demand-supply dynamics remain a risk for medium to long-term bond yields.

Portfolio Positioning

In the Quantum Dynamic Bond Fund, we have been avoiding long-term bonds for some time due to our cautious stance on the markets. The defensive positioning helped the portfolio ride through the market sell-off over the last three months.

After the steep sell-off in the last two months, valuations have become even more attractive on medium to long-term bonds. However, given the high uncertainty as mentioned above, we will continue to be cautious in adding long-duration bonds as a core portfolio position.

We used the recent rise in bond yields to deploy the portfolio cash into 3-5 years government bonds. For the core portfolio, we continue to like the 3-5 years maturity bonds, which in our opinion offer the critical balance between duration and accrual yield.

We would remain open and nimble to exploit any market mispricing by making a measured tactical allocation to any part of the bond yield curve as and when the opportunity arises.

We stand vigilant to react and change the portfolio positioning in case our view on the market changes.

What should Investors do?

After more than a 100 bps sell-off in the bond market over the last year, the return potential of debt funds has improved significantly. We suggest investors increase allocation to dynamic bond funds in a staggered manner with 2-3 years holding period.

Investors with a shorter holding period and low-risk appetite should stick to liquid/money market funds with low credit risks.

For any queries directly linked to the insights and data shared in the newsletter, please reach out to the author – Pankaj Pathak, Fund Manager – Fixed Income at [email protected].

For all other queries, please contact Neeraj Kotian – Area Manager, Quantum AMC at [email protected] / [email protected] or call him on Tel: 9833289034

Read our last few Debt Market Observer write-ups -

- RBI Sprint - Market Tremors

- Inevitable Pivot: Resetting Market Expectations

| Name of the Scheme | This product is suitable for investors who are seeking* | Riskometer |

| Quantum Dynamic Bond Fund An Open-ended Dynamic Debt Scheme Investing Across Duration. A relatively high interest rate risk and relatively low credit risk. | • Regular income over short to medium term and capital appreciation • Investment in Debt / Money Market Instruments / Government Securities |  Investors understand that their principal will be at Low to Moderate Risk |

| Potential Risk Class Matrix – Quantum Dynamic Bond Fund | |||

| Credit Risk → | Relatively Low | Moderate (Class B) | Relatively High (Class C) |

| Interest Rate Risk↓ | |||

| Relatively Low (Class I) | |||

| Moderate (Class II) | |||

| Relatively High (Class III) | A-III | ||

The views expressed here in this article / video are for general information and reading purpose only and do not constitute any guidelines and recommendations on any course of action to be followed by the reader. Quantum AMC / Quantum Mutual Fund is not guaranteeing / offering / communicating any indicative yield on investments made in the scheme(s). The views are not meant to serve as a professional guide / investment advice / intended to be an offer or solicitation for the purchase or sale of any financial product or instrument or mutual fund units for the reader. The article has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate and views given are fair and reasonable as on date. Readers of this article should rely on information/data arising out of their own investigations and advised to seek independent professional advice and arrive at an informed decision before making any investments.

Please visit – www.quantumamc.com/disclaimer to read scheme specific risk factors. Investors in the Scheme(s) are not being offered a guaranteed or assured rate of return and there can be no assurance that the schemes objective will be achieved and the NAV of the scheme(s) may go up and down depending upon the factors and forces affecting securities market. Investment in mutual fund units involves investment risk such as trading volumes, settlement risk, liquidity risk, default risk including possible loss of capital. Past performance of the sponsor / AMC / Mutual Fund does not indicate the future performance of the Scheme(s). Statutory Details: Quantum Mutual Fund (the Fund) has been constituted as a Trust under the Indian Trusts Act, 1882. Sponsor: Quantum Advisors Private Limited. (liability of Sponsor limited to Rs. 1,00,000/-) Trustee: Quantum Trustee Company Private Limited. Investment Manager: Quantum Asset Management Company Private Limited. The Sponsor, Trustee and Investment Manager are incorporated under the Companies Act, 1956.

Posted On Friday, Apr 21, 2023

The fiscal year 2022-23 has come to an end. The defining feature

Read More

Posted On Thursday, Mar 23, 2023

Indian money markets have tightened meaningfully over the last one and a half month.

Read More

Posted On Friday, Feb 24, 2023

Inflation has been one of the biggest challenges in the post-pandemic world.

Read MoreGet In Touch

Take small steps in your financial planning to achieve big dreams! Start your investment journey today!